|

|||||||||||||||||

|

[Please open the attached .pdf for best viewing.] By William Ribaudo

Stealth Japan: The Surprise Success of the World's First InfoMerc Economy, by Scott Foster Or purchase on Amazon.com And -

Get the source material behind the most-viewed 60 Minutes investigative episode in history, until now a Cabinet-level briefing book, on the world's most important information: how does China make its money, at what cost to the world, and what happens next?

Publisher's Note: Most of us view companies - and assess their value - through an informal combination of what they make, who runs them, the size of their markets, and, all too often, what others are thinking that week. In this week's issue, Deloitte's Bill Ribaudo expands upon a theme he first shared with us at FiRe. Just as we at SNS have learned over time to view countries in terms of their business models, Bill has now made the case that companies are valued by Wall Street in the same way. Whether you are an investor, a manager, or a startup founder, the information Bill shares in this week's issue will both ring true and help you refine how you look at - and value - your own ideas, plans, and company. We think these ideas are as revolutionary as they are sensible, and we encourage all members to spend the time to see the business, and technology, world through these new eyes. - mra.

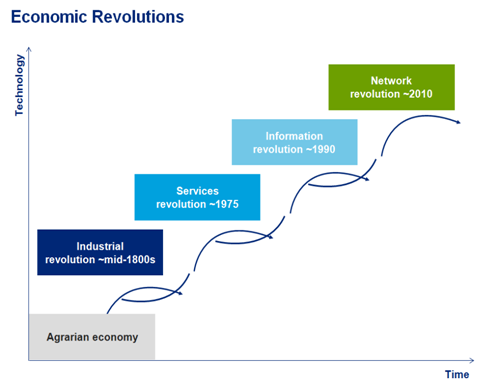

Technology Is Changing How We View Industry, By William Ribaudo Across the economy, industries are converging, driven by now-ubiquitous technology that is redrawing - and in some cases erasing - traditional market boundaries. Rapid innovation is creating space for new business models to emerge in almost every industry. And both of these trends are being accelerated by an influx of capital from private equity firms and Wall Street, driving higher company valuations. Examples of technology convergence can be found in almost every industry. Is Airbnb a hospitality business, or is it a technology platform? Is Uber a technology company, or is it a travel and transportation business? Are eBay and Amazon, with their large e-commerce presences, really retailers, or are they online technology platforms? Is Tesla an automotive company, or a technology company that creates energy, software, and hardware and puts it on four wheels? According to its website, Tesla is not only an automaker, but is also a technology and design company with a focus on energy innovation. As traditional industry delineations become less clear, we've heard some analysts say that all companies will become technology companies. Others like to think that technology as an industry will disappear, becoming part of all other industries. Still others predict that the physical will be replaced by the virtual - or the virtual will crash, leaving only the physical. What do I think? I believe that technology will collide further with all other industries, making traditional industry classification less and less relevant. That the physical and virtual, the tangible and intangible, will coexist and balance. The challenge, as I see it, lies in avoiding as much carnage as possible on the way to eventual equilibrium. And we've endeavored to help determine which entities will flourish, survive, or cease to exist amid what we call The Great Race. In business, the traditional sources of value creation have been clear and intuitive for decades: create a product or service that the market demands, and sell it for a profit. Investors have recognized this approach to business and valued companies based on their ability to make a profit given a certain set of (typically physical) assets. In today's economy, however, we're seeing a new kind of company, one that is valued differently; companies that have yet to turn a profit have market capitalizations into the billions. Today, investors are measuring, and rewarding, value very differently than they have in the past - and we believe that such valuation is neither a bubble nor a fad. LinkedIn has 430 million users[1] and a market capitalization of $16 billion[2]; in addition to its subscription business model, it operates as an essentially free professional recruiting and networking service. Approaching a market capitalization of $500 billion,[3] Google provides Internet-related searches and other services - for free. Both companies produce profits from established advertising-based revenue models, yet their valuations suggest something more there than current revenue and profits. How can these companies, with their limited physical assets, be worth so much? What is it that investors are rewarding? These questions guided our research, and the resulting insights can help management teams understand the value shift underway. The Four Great US Economic Revolutions (So Far) There have been four great US economic revolutions since the 19th century (see Figure 1). New technology sparked each revolution, and each in turn spawned an entirely new business model. These new models have repeatedly changed many things - from how, when, and where value is created to the key performance indicators (KPIs) that businesses and investors use to measure performance. Figure 1. US economic revolutions

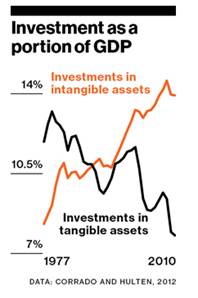

Copyright 2016 Deloitte Development LLC The Industrial Revolution During the Industrial Revolution, the US economy transitioned to new manufacturing processes, moving from hand production to machines. The industrial mindset was capital-intensive, with asset or factory utilization and return on physical assets the measurements of performance and value. The Services Revolution In the mid-1970s, US corporations determined that businesses could service what they sell, using a lower-capital-deployed / lower-risk model to yield higher returns. This birthed a new services-driven business model, under which a company's primary measure of performance and value is employee utilization. The Information Revolution Around 1990, the birth of the modern Internet, along with the rapid advancement of global and mobile communications, changed almost everything once again. The Information Revolution was characterized by a shift to a high-tech, knowledge-driven global economy - one based on information, computational speed, and processing capability. Value moved from hard to soft assets, physical to intellectual, tangible to intangible. Performance measures and KPIs changed as well, with investors keen on tracking return on R&D investment. Over the past few decades, companies have been investing more in development of intangible assets and less in tangible assets, as shown in Figure 2. Figure 2. Tangible vs. intangible assets: Investment trends[4]

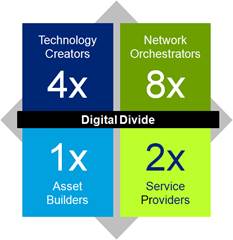

The Network Revolution By 2010, companies had begun tapping into larger networks, driving yet another rapid shift in value creation. In the Network Revolution, we find companies generating value based on relational links to customers, suppliers, and other contacts. Investors now watch KPIs that track numbers of and return on relationships, connections, and interactions. Valuation in the Information Age Deloitte collaborated on research on a 40-year lookback of data from the S&P 500 companies. We're seeing a new trend of companies being valued differently. It's clear that in recent years investors have been measuring and rewarding differently than they have in the past. Internet, social media, mobile, and cloud computing have removed many traditional barriers to growth, opening up new markets with the click of a mouse. Within this expanded business ecosystem, companies can analyze faster, ship faster, and hire faster. In determining how to view differentiated value, we looked first at price-to-revenue ratios (P/R), in part because revenue is a more stable and more predictable measure, less susceptible to high variation. We also became aware of a trend in which, as companies become digitally enabled, they trade more on revenue performance than on earnings performance. After choosing price per revenue as a metric, we looked at how company valuations have changed over time. After examining 40 years of financial reports for the companies in the S&P 500 index, and analyzing which received the highest P/R valuations, we found a strong correlation between valuation and business model. What we learned after evaluating each company's business model was remarkably simple - and it helped us deal with the complexity of industry sector convergence. A New Framework Emerges: Business Model Is the New View Our research identified a new way to view companies, through a business-model lens. We identified four foundational business models, the differences among them based largely on companies' management preferences and investment strategies. As our interest in business models deepened, we asked what the companies with the highest P/R (which we call their Revenue Multiplier) have in common. One thing we noticed was the pervasiveness of digital technologies across industries, sectors - and yes, business models. Here's a representation of how one can think about the four business models:

The Revenue Multiplier Effect and the Digital Divide Each of the four business models we examined turned out to yield significantly different Revenue Multiplier results. In particular, Technology Creators and Network Orchestrators were valued two to four times as much as Asset Builders and Service Providers; we call this advantage the Revenue Multiplier effect. On average, the market pays approximately $8 of valuation for every $1 in revenue generated by a Network Orchestrator company. Asset Builder companies, meanwhile, receive only $1 for every $1 in revenue (see Figure 3). The presence and importance of technology within a business model has created a "digital divide." Asset Builders and Service Providers fall below the divide, and Network Orchestrators and Technology Creators are above it. These latter technology-based business models grow faster, scale faster, and have higher Revenue Multipliers. And the higher overall Revenue Multiplier for tech-enabled companies indicates that investors (who ultimately pay for the prospect of future earnings) recognize the value of technology and reward businesses that have the ability to grow faster. Figure 3. Revenue Multipliers above and beyond the digital divide

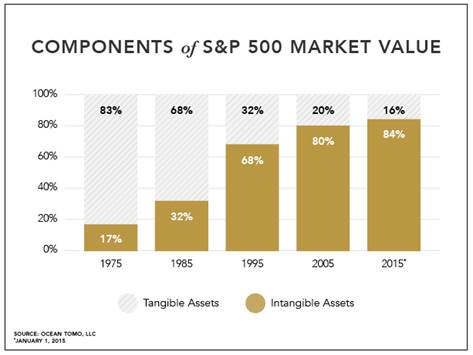

Financial Markets Shift to Intangible Assets Another way to understand relative valuation changes is to look at the components of stock market value, and how valuation has shifted over time. From 1975, at the beginning of the Services Revolution, to 2010, the start of the Network Revolution, the major component of the market value of the S&P 500 shifted dramatically from physical to intangible. In 1975, for a subset of 300 S&P companies, 83 percent of market value was related to physical assets such as factories, equipment, and inventory - all recorded on companies' balance sheets as net book value. Market capitalization was close to book value, because fixed or tangible assets made up the majority of a company's value. But by 2015, only 16 percent of market value in the analyzed group was related to net book value or tangible assets. An overwhelming 84 percent of value was represented by intangible assets such as intellectual property and customer capital, as shown in Figure 4. Figure 4. Tangible vs. intangible assets as components of market value[5]

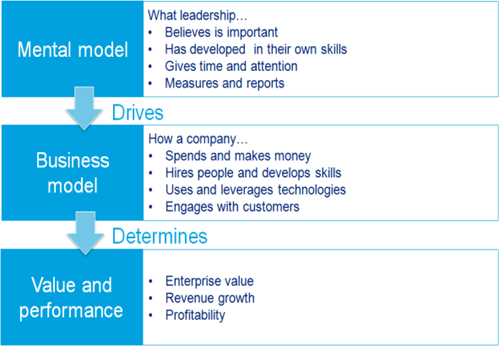

In today's paradigm, we all must adjust our view of assets to encompass intangible assets - including those that the market values but that are not on the balance sheet. With this new perspective, management can begin to look toward shifting business models to monetize these (now more visible) intangible assets and further grow a business's overall value. Mental Models Dictate Business Models Many corporate leaders have built long, successful careers managing companies in a particular industry - working from assumptions, behaviors, and beliefs that have guided them and their organizations for decades (see Figure 5). By the time such people occupy the top ranks of an organization, they have become specialists at managing a particular business model, with preferences for time and capital allocation tuned to the needs of the business. They intuitively invest in the asset types (e.g., fixed assets, people, IP, or networks) that create value and support their particular business models. Successfully introducing a new business model to an organization requires a mental shift - and changing mental models isn't easy. It takes conscious, concentrated effort to see and cultivate value in an area that a business has previously ignored, to ensure stakeholder buy-in, and to use it to drive success. Figure 5. Mental business models and their effects

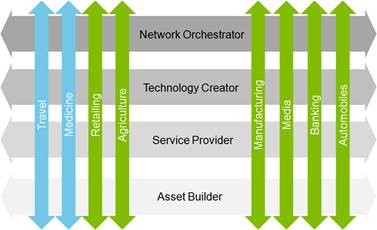

Vertical Industries Include a Growing Variety of Business Models Within almost every industry, one can find examples of Asset Builders, Service Providers, and Technology Creators; it's fair to say that more industries than not include at least two of these business models (see Figure 6). Most recently, Network Orchestrators have emerged to shake up many industries - and to add yet another model to the mix. One prominent example is the taxi and hired-car industry. It has long encompassed Asset Builders (the auto manufacturers) and Service Providers (the taxi or coach companies that own and operate the vehicles), as well as Technology Creators (reservation companies that dispatch captive drivers using technology). Most recently, the industry has been massively disrupted by the rise of Network Orchestrators, such as Uber and Lyft, that will pay anyone who meets their criteria to drive his or her own car for hire - and offer any app-using rider a car on demand. Figure 6. Vertical industries span multiple business models

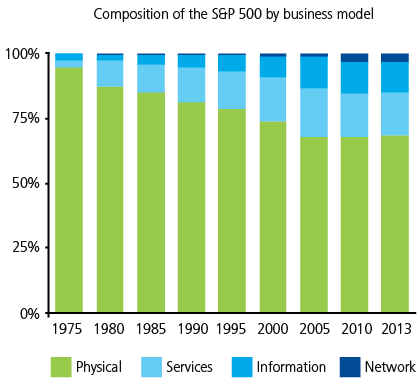

Business Model Transformation: The Key to Exponential Growth With increasing variation of business models across and within industries, a company's business model is more closely tied to its potential for value. A management team can increase the value of its business in three ways: linear, step, and exponential. The first two options are well understood: to drive linear growth in P/E, management must find ways to create additional profits and revenue or to meet or beat market expectations. A company can also acquire a lower P/E company, fold it into the higher P/E company, and leverage up the acquired business's P/E - generating step P/E growth. But the biggest opportunity lies in exponential growth. If management can successfully move a company's business model - for example, shifting the business from an Asset Builder toward a Technology Creator or a Network Orchestrator - they can exponentially expand the business's Revenue Multiplier and shareholder value. Sounds easy - but it isn't. However, it is possible. In the last few years, we've seen just a few companies make significant changes to their business models, then reap the rewards of the resulting increases in Revenue Multiplier and shareholder value. Under Armour, for example, spent close to $1 billion buying fitness-related mobile apps and bringing a biometric fitness device to market. These plays above the digital divide helped grow its Revenue Multiplier from 3.2x to 5.6x in three years. Similarly, another noted sportswear company increased its Revenue Multiplier from 1.4x to 3.0x in the last nine years by aggressively pursuing technology "as" the business as well as "in" (i.e., supporting) the business. Although the composition of the S&P 500 has changed significantly over the years, there are still plenty of companies that have an opportunity to increase their Revenue Multipliers by moving toward information- or network-based business models (see Figure 7). Figure 7. Composition of the S&P 500 by business model

Note: Based on analysis of the S&P 500 Five Practical Steps for Increasing Value In the last two decades, driven largely by digital technologies and massively increased connectivity, the global economy has moved beyond narrowly defined industries built around large, vertically integrated, and mainly self-contained corporations. New means of creating value are being developed everywhere, in the form of ever-denser, ever-richer networks of connection, collaboration, and interdependence. And businesses around the world are adapting - or being left behind. The rise of business ecosystems is fundamentally altering key success factors for many leading organizations, forcing them to think and act very differently about strategies, business models, leadership, organizational structure, core capabilities, and value creation and capture - in short, changing their mental models. We've identified five practical steps that management can take to increase value through business model transformation: understand, create, develop, reallocate, and formulate. 1. Understand. The first step: Understand yourself and the company within the larger landscape, including your mental model as well as your current business model. Gather your executives to examine your company values, identify performance measures, and calculate your Revenue Multiplier. 2. Create. Next, assemble a new market-based balance sheet, including a complete inventory of intangible, relationship, and network assets. Determine the dollar value of any gap separating the value of net assets on the balance sheet and the value investors place on your business. Allocate the value of the gap to those assets that you have identified, but that are not on the balance sheet. 3. Develop. Identify which intangible assets (e.g., IP, employee knowledge, customer "stickiness," customer data) are worth additional investments or can be used to develop new business models that would unlock their otherwise latent value. 4. Reallocate. Create a plan to reallocate more of your capital to those identified intangible assets that support business models above the digital divide. 5. Formulate. You can manage only what you measure. As you develop new business models and reallocate capital, you'll want to add new KPIs that support those models, and align incentives to reinforce them. To enhance value recognition by the markets, you'll also want to consider your future portfolio and capital structure. Reevaluate your portfolio structure, investment plans, and acquisition priorities by business model. Then as business models reach scale, consider alternate capital structures to recognize created value - for example, a partial or full spinoff. What It Will Take to Win the Great Race In 2013, when we completed our research and began articulating the results, many of the concepts we discuss here were not yet widely understood; many corporate leaders were still operating under an Industrial Revolution mindset. But in the last few years, the pace of change has accelerated and become more evident - and more and more companies are acting in ways consistent with our business-model viewpoint. Industrial giants are exploring how to harness the Internet of Things, building a rejuvenated industrial ecosystem that relies on information culled from connected devices to generate smarter decisions on everything from product design to energy usage. At the same time, industries are converging at a rapid rate, and traditional industry boundaries are blurring. Manufacturers are mining data and generating insights from connect devices while software companies invest in storefronts and expanded campuses. Amid such intense change, some (but not enough) Asset Builders and Service Providers are striving to transcend the digital divide by harnessing technology, leveraging customer or supplier data, or orchestrating networks to transform themselves toward Technology Creators or Network Orchestrators - driving higher Revenue Multipliers and shareholder value. Meanwhile Technology Creators and Network Orchestrators are eyeing physical assets that can round out their offerings. There is no single solution to winning the Great Race. In the end, it's about using today's technology to build businesses that meet customers' needs. The businesses that dominate tomorrow's landscape will be those that blend the physical and virtual to win the Great Race - while those that remain one-dimensional are likely to struggle. _____ Seema Bajaj contributed to this article. [1] About LinkedIn, https://press.linkedin.com/about-linkedin, accessed May 2, 2016. [2] LinkedIn Corporation (LNKD), https://finance.yahoo.com/q?s=LNKD, accessed May 2, 2016. [3] Google Finance, "Alphabet Inc. (NASDAQ:GOOG)," https://www.google.com/finance?q=goog&ei=tJYyVoCpHKz5igLK8qTgAw, accessed April 4, 2016. [4] Bloomberg, "The Rise of the Intangible Economy: U.S. GDP Counts R&D, Artistic Creation," https://www.bloomberg.com/news/articles/2013-07-18/the-rise-of-the-intangible-economy-u-dot-s-dot-gdp-counts-r-and-d-artistic-creation, accessed April 22, 2016.

Bill is a frequent author and speaker on digital business model innovation and its link to market valuation. Recently he was published in the Wall Street Journal, Knowledge@Wharton, and Deloitte CFO Insights. Some recent media interviews and speaking engagements include the 10th Annual Utah Economic Summit, 2015 Future in Review (FiRe) conference, Business Radio on Sirius XM powered by the Wharton School, The McCuistion Program on PBS, and the Dallas Annual Governance Symposium at the University of Texas. Bill is part of Deloitte's US CFO Program leadership team and serves as the managing partner and dean of The Next Generation CFO Academy.

Seema Bajaj leads marketing and eminence efforts for Deloitte Advisory's Technology, Media, and Telecommunications (TMT) Industry. She works closely with the leadership team to identify and drive strategic initiatives to build Deloitte's brand in the marketplace. Seema has broad experience in integrated marketing, business development, and strategy. Her professional experience includes marketing and business development roles within the legal industry and other professional services firms. This document contains general information only and Deloitte is not, by means of this document, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This document is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte Advisory shall not be responsible for any loss sustained by any person who relies on this publication. As used in this document, "Deloitte" means Deloitte & Touche LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

I would like to thank Bill for making the effort to condense his intensive study of this subject into the length of a Special Letter, and for working with all of us at SNS on a related project we will be releasing at Future in Review 2016. - mra. I also want to thank Editor-in-Chief Sally Anderson for putting all of these thoughts into perfect shape.

Your comments are always welcome. Sincerely, Mark R. Anderson

To arrange for a speech or consultation by Mark Anderson on subjects in technology and economics, or to schedule a strategic review of your company, email mark@stratnews.com. We also welcome your thoughts about topics you would like to suggest for future coverage in the SNS Global Report.

Please visit www.stratnews.com/insideSNS for:

Register now for FiRe 2016, our 14th annual Future in Review conference September 27-30, 2016 At the Five Diamond Stein Eriksen Lodge, Deer Valley In Park City, Utah At www.futureinreview.com/register

With great appreciation for our SNS Global Platinum Partners

Our Global Silver Partner

And our SNS Computing and Communications Channel Partners, Telstra and Everyone Counts:

Our FiRe Global Initiatives Channel Partner, Haydale:

And our Healthcare Channel Partners, Simavita and Harris & Harris Group:

... for their Partnership and Support of SNS Events.

Thank you to our FiRe Bronze Partners, Deloitte and Microsoft

And Additional Supporting Organizations

FiRe/Thunderbird Internship Sponsor

FiRe Academic Partner

* On September 27-30, Mark will be hosting the 14th annual Future in Review conference, at the Stein Eriksen Lodge in Park City, Utah. To register for FiRe 2016, featuring work on "The Power of Flows," go to www.futureinreview.com.

Copyright 2016, Strategic News Service LLC "Strategic News Service," "SNS," "Future in Review," "FiRe," "INVNT/IP," and "SNS Project Inkwell" are all registered service marks of Strategic News Service LLC.

ISSN 1093-8494 |

Visit the SNS Store to check out the first of our SNS FiReBooks imprints!

Visit the SNS Store to check out the first of our SNS FiReBooks imprints!

As a managing partner with Deloitte & Touche LLP, Bill Ribaudo leads its Technology, Media, and Telecommunications Industry practice and is a senior advisory partner to some of Deloitte's most strategic TMT clients. He has over 30 years of business experience, including public company executive financial management and strategic and operational consulting.

As a managing partner with Deloitte & Touche LLP, Bill Ribaudo leads its Technology, Media, and Telecommunications Industry practice and is a senior advisory partner to some of Deloitte's most strategic TMT clients. He has over 30 years of business experience, including public company executive financial management and strategic and operational consulting.