|

|||||||||||||||||

_______ Coming April 23! With Special Guest The Honorable John C. Demers Assistant Attorney General

"Spy vs. You:

Interviewed by Evan Anderson, CEO, INVNT/IP (Subject of 60 Minutes' "The Great Brain Robbery") Reception, Talks & Dinner, starting at 5:30pm Lotte New York Palace Hotel

How a climate of financial instability is driving unprecedented global losses in the insurance and reinsurance industries by Berit Anderson While politicians and lobbyists argue endlessly about whether climate change is human-caused, there is one industry in particular already feeling the financial burden of global climate change: homeowners insurance.

Insurance companies around the world suffer direct financial impact whenever a wildfire swoops across Australia or Northern California or a hurricane makes its way up the Eastern Seaboard. And, although most people don't realize it yet, the numbers at these companies provide perhaps our most accurate real-time indication of the global impacts of climate change. In fact, things have gotten so dire in home insurance that we feel it merits its own discussion as an industry. If your house burns down, you rely on your insurance policy to rebuild. But what happens when everyone's house is burning down, as in the case of California, South America, and Australia?

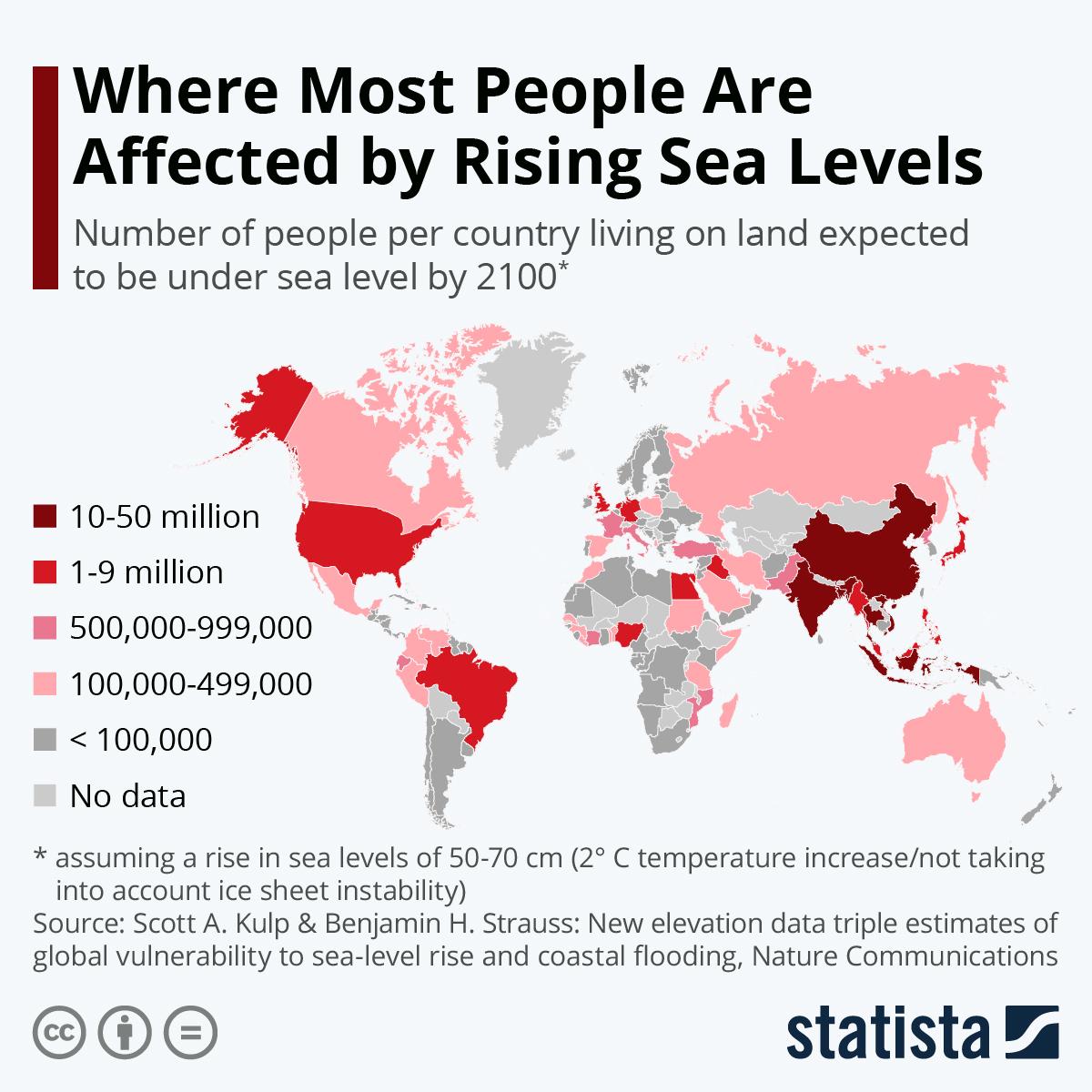

Mean July Fire Weather Index from 1980-2012, based on the Chen et al. (2008) daily precipitation estimate over land. Figure created using the Panoply desktop application. Or flooding, as in the case of India, China, and Alaska? Or being slowly swallowed by sea-level rise, as in the case of Northern Europe, Florida, the East Indies, and wide swaths of the eastern and southern US seaboard?

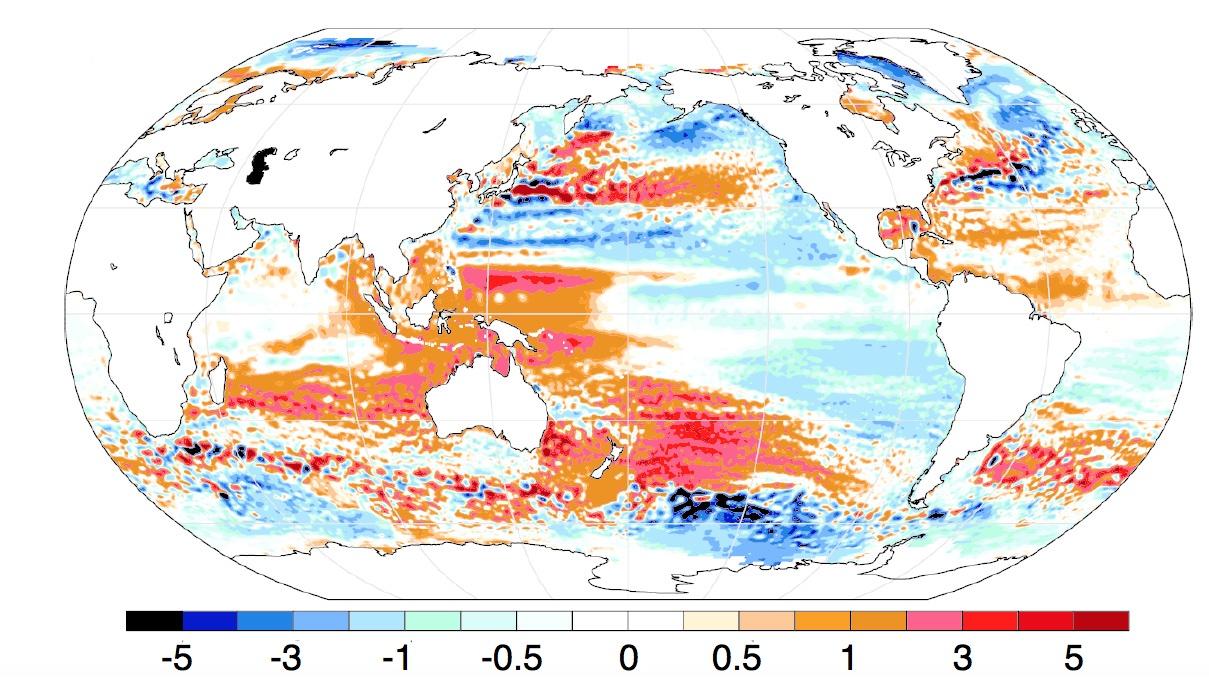

Regional sea-level trends in millimeters per year from 1993 through mid-2018 with the global average rate removed. Red colors indicate that the local rate of sea level rise was greater than average, and blue colors indicate the opposite. (Image: PNAS) Insurance as a business proposition has historically worked because mean risk has decreased as the number of insured sample size increased. But what happens when global risk suddenly balloons to unprecedented levels? What happens when the entire global home stock falls victim to a surge in fire, flooding, hurricanes, and sea-level rise? Well, let's take a look at the global home insurance market. Delayed Reaction: The State of Insurance

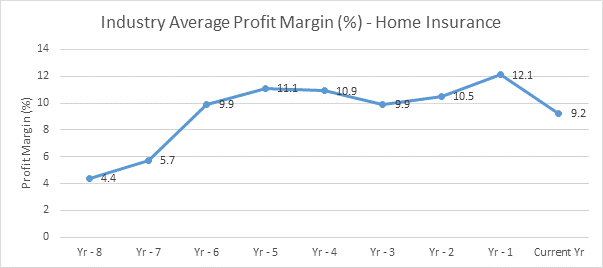

Average UK broker profit margins in home insurance. Current year = 2018. (Credit: Plimsoll Publishing Ltd) At first glance, recent figures don't seem catastrophic - at least not relative to those of some earlier years they're often compared with. But the deeper you look into the insurance and reinsurance industries, the more complicated the news gets. That's because - at least initially - homeowners insurance losses aren't reflected in the balance books of insurance companies, but rather in the books of those companies' reinsurers. Which means that industry analysts have been making rosy, albeit imprecise, predictions like the one shown below, based on global need for insurance and large markets opening up in developing countries that don't take into account the coming burden from climate-change-based reinsurance losses.

Further obscuring the real story is that home insurance premiums have gone up - significantly - increasing initial financial cover for companies that provide homeowners insurance.

The problem is, as global catastrophe rises in the form of natural disasters, so too do claims. But insurance companies have so far been shielded from the full weight of these losses by their own insurance - the reinsurance industry. Reinsurance: The Canary in the Coal Mine So what's happening in the reinsurance industry today? In April 2019, an article in the Financial Times already warned that "[p]rofitability at some of the world's biggest reinsurance companies has more than halved over the past five years, according to research, in a sign of the huge pressure facing the industry. Willis Re, a reinsurance broker, said the annual return on equity at a selection of major reinsurers fell from 6.7 per cent in 2013 to just 2.7 per cent last year, after taking out the impact of major natural catastrophes." But let's not take out the impact of major natural catastrophes. Since they are the whole story. As Aon Securities put it in its September 2018 report, "Insurance Linked Securities": 2017 marked the second costliest year ever recorded for natural disasters, at USD353 billion. USD220 billion, or 66 percent, of losses came from just three hurricanes: Harvey, Irma, and Maria. The losses from these disasters were 66 percent higher than the 16-year median annual loss of USD132 billion, while total 2017 losses were 93 percent higher than the average for the 21st century. Catastrophe activity led to insured losses that were 163 percent higher than the 2000-2016 average. This led to economic losses in excess of USD300 billion, surpassed only by the economic losses of 2011. Sixty-two percent of this economic loss came from just three storms during one of the costliest Atlantic Hurricane seasons. Adding to this substantial loss was the most destructive wildfire event ever recorded in the state of California, which caused USD13 billion in damages last October. Furthermore, USD12 billion in losses were recorded due to flooding in the Yangtze River Basin in China, while two earthquakes in Mexico caused a cumulative USD6 billion in damages. Property & Casualty Reinsurance reported a net income for 2018 of USD 370 million compared to a net loss of USD 413 million in 2017. Both years were affected by large natural catastrophe losses, while 2018 also saw a significant impact from large man-made losses. Estimated total large natural catastrophe and man-made losses amounted to USD 2.3 billion in 2018, mainly stemming from the Ituango dam collapse in Colombia, the Camp and Woolsey wildfires in California, hurricanes Michael and Florence in the Americas, floods and winter storms in Japan, also hit by typhoons Jebi and Trami, the Sydney hailstorm and a fire at a shipyard in Germany. The net operating margin was 4.3% in 2018, up from -1.3% in 2017. [Note that this report was created before the wildfires of 2019-2020 in California and Australia, continuing earthquakes in Puerto Rico, and ongoing floods in the US.] As stated by the Insurance Information Institute's 2018 year-end year-end industry report on reinsurance: "Results were good in comparison with 2017 - but 2017 was a horrible year." Depending on their individual risk-modeling capabilities and exposure to homeowners insurance, we can expect the below firms to continue to take serious hits.

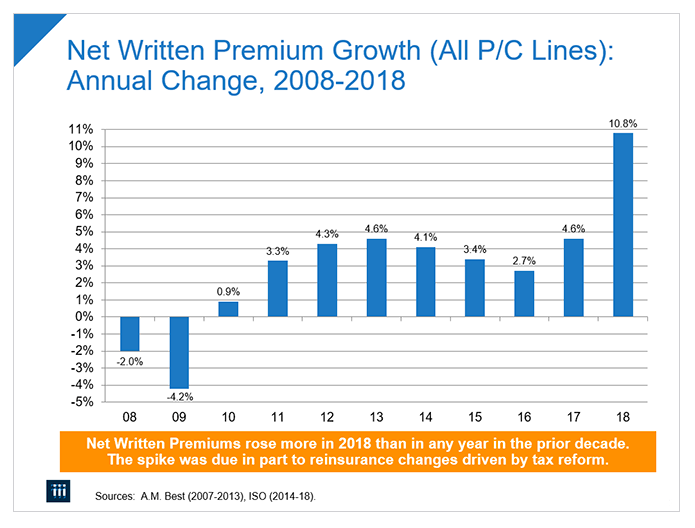

The Changing State of "Cat Bonds" So why isn't this hitting the insurance industry itself yet? A few reasons. In 2018, US reinsurers benefited from a surge in net written premiums driven by tax reforms.

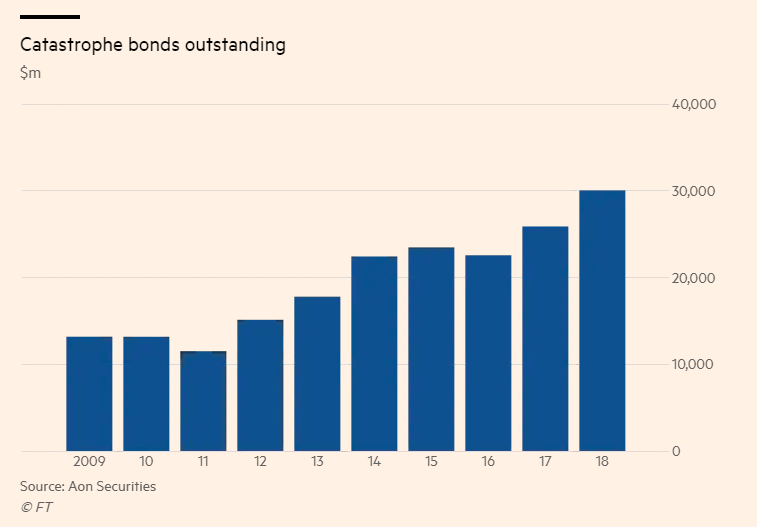

At the same time, private investment flooded the market in the form of catastrophe bonds:

Generally, catastrophe bonds - or "cat bonds," as they're known in industry parlance - have served as insurance for the reinsurance industry: a way of offsetting reinsurance risk by extending liquidity through private investors. As worries about the stability of global stocks proliferated throughout the investment world, cat bonds had a reputation for relative stability, with a general YOY return of about 7%. And with IPOs of overvalued companies floundering, the prospect of an asset-class not tied to other financial markets became even more attractive. Between 2013 and 2018, the volume of outstanding catastrophe bonds ballooned to an unprecedented $30B, according to research from Aon Securities. However, as global climate catastrophes have become more widespread, the recent spike has been driven at least partially by a sudden upsurge in government-issued cat bonds. For example, 2018 saw the largest-ever cat bond - the $1.4B Pacific Alliance bond - issued by the World Bank to protect Chile, Colombia, Peru, and Mexico from earthquake damage. In other words, at the exact moment that reinsurance prices should have taken a steep hike based on increasing claims and underlying market conditions, two sets of temporary circumstances artificially pushed them down. But all that glitters is not gold. And the market for cat bonds is due for a reckoning. As Financial Times insurance correspondent Oliver Ralph reported in September 2018: "The costs from natural catastrophes have dented returns for ILS and cat bond investors. Aon's ILS index returned 2.7 per cent last year, half the level of 2017. Over the past 10 years, the index has returned an average of 6.5 per cent a year." So far, private investors have yet to respond meaningfully to this sudden drop (more than half) in cat bond returns. And while returns for individual cat bonds may vary year-to-year, there's no sign that the overall downward trend will change. Eventually, that 2.7% will drop to 2% and then to 1.5%, with cat bond investors the frogs sitting placidly in the boiling pot. But while private investors may be sitting tight, the data-backed, algorithmically obsessed reinsurance companies, driven by complicated risk models, are not. There has been a sudden boom of mergers-and-acquisitions activity, with reinsurance companies buying cat bond brokers, trying to arbitrage profit from the slower-moving private investors. They've also been snapping up smaller reinsurance providers, increasing their efficiencies of scale and doing their best to wring the last few drops of water out of the old insurance rag - the larger the sample size, the less the overall risk. But that model is broken. The risk is now (nearly) everywhere. So it's not surprising that in 2019 reinsurance prices rose steeply. According to the above-linked Financial Times article, "[d]uring the April contract renewal season, rates in some areas, especially those affected by losses last year, rose up to 25 per cent, according to Willis Re. early signs from the June renewal season were also good. June renewals are closely watched as they include contracts in Florida, which is often hit by severe storms." Which means that further shock in the home insurance industry is not far behind. Signs of Coming Trouble for Insurance Already, California homeowners living in "high-risk" areas are being priced out of their premiums or dropped from their plans entirely. "A California Department of Insurance report found that the number of homeowners in the wildland-urban interface who complained about getting dropped by their plans more than tripled from 2010 to 2016," the LA Times reported in August of 2018. "Complaints about increased premiums rose 217%." It's estimated that 1 million California homes are considered at high risk for wildfires - a group that is increasingly uninsurable by traditional providers. And that's only one US state. In Florida, which boasts the highest home insurance premiums of any state in the US, up to 18 insurance companies are facing financial-strength ratings downgrades sometime this spring according to a letter written by the president of ratings agency Demotech. Because federally backed mortgage lenders only accept insurers with "A" ratings from the agency, all 18 of those companies must either recapitalize or seek acquisition opportunities. Otherwise, their customers will have to find new providers. Meanwhile, in Australia, the unprecedented wildfires of 2019-2020 have put further strain on insurers. According to a January 23, 2020, statement from the Insurance Council of Australia (ICA), approximately 20,000 claims have been issued since the start of the 2019 wildfire season, with an estimated value loss of $1.65 billion. That number is expected to rise. "Despite the manageable impact for insurers, the catastrophic fires highlight that the P&C [Property & Casualty] insurance industry is at the forefront of environmental risk," Frank Mirenzi, a Moody's vice president and senior credit officer, told Insurance Business Magazine in January. "The industry is exposed to the economic consequences of climate change, primarily through the unpredictable effect of climate change on the frequency and severity of weather-related catastrophic events, such as hurricanes, floods, convective storms, drought, and wildfires." Australian PM Scott Morrison may be too politically insecure to blame wildfires on climate change, but Moody's certainly isn't. According to their estimates in the same article, Australian insurers Suncorp Group (through its subsidiary AAI) and IAG will likely receive the largest sum of gross claims, although QBE, Allianz SE, and Zurich Insurance Co. will also be adversely affected. A report issued

by the Australian firm Climate Risk even prior to this year's catastrophic fires projected that the number of "uninsurable" addresses in Australia would double by the turn of the century to nearly 720,000 - or one in 20. Thousands more homeowners, they predicted, will see their premiums double or triple within decades. Where else will homeowners insurance become an unsustainable business prospect? Well, we can start by revisiting the three figures at the beginning of this piece. The frightening thing, from both a human- and financial-risk perspective, is that when we overlay maps of global flooding, hurricane damage, sea-level rise, and fire destruction on top of one another, we're left with a rather glaring truth: There are very few places on Earth that will continue to be "insurable," by traditional business definitions. A few weeks ago, Tim O'Reilly, founder and CEO of O'Reilly Media, shared his thoughts on the power of climate change to transform the economy in a conversation with Sam Lessin of technology website The Information: "I think our fundamental perception of what matters in the economy is going to shift. And where market power goes," he said. "I mean Elon Musk is probably the first, most-visible climate billionaire. He basically made this big massive bet on the transformation of electric vehicles and he did catalyze it and did market it. And, you know, there are people doing that with areas like how do we get off of meat? The new fortunes, I don't think are going to be in places like VR or consumer tech or entertainment. I think that the urgency of the economic shifts that are coming at us are going to radically change our perspectives on what we have to do and where investment has to flow." The insurance industry is on the front lines of this trend O'Reilly describes. At some point, particularly in uninsurable areas, the growth line of skyrocketing insurance premiums will cross the declining line of consumers' expendable income, effectively negating the ability of all but the wealthiest homeowners to afford homeowners insurance. If and when that happens, insurers will be faced with some very existential questions: How do you make a business out of insuring anyone with global risk and payouts skyrocketing? How do you decide what areas are still insurable? At what cost to homeowners? How will this trend affect home ownership rates, particularly by millennials and Gen-Z, who are already opting or being priced out of home ownership? And, perhaps most important, how do you reinvent an industry built on an assumption of distributed risk that is no longer accurate? Are we facing the end of homeowners insurance? What the increasing losses and risks of the insurance and reinsurance industries make clear is that we don't need to argue about the politics of climate change. All we need to do is read the news every morning for updates on the latest wildfire, check our home insurance prices, and follow the stock market. In the short term, you can expect catastrophe bonds to become, well, a catastrophe, as governments max out their ability to guarantee bonds; reinsurance company losses to flatten somewhat as price increases finally catch up with climate change and the buck is passed to the insurance industry; and the insurance industry itself to enter a sustained nosedive. Oh, and by the way, if you own a home, you might want to start saving for your future premiums. The sky's the limit.

Mark Anderson contributed research direction to this article.

An international keynote speaker and advisor on innovation, technology, media, and global policy, Berit has appeared at the Brussels Forum, the European Council on Foreign Relations, the Conference on World Affairs, TEDxVilnius, DevoxxBelgium, and TEQNation, among others. In 2017, her work on information warfare was featured in the New Yorker, Gizmodo, and TechCrunch, and cited by internet creator Tim Berners-Lee as one of the top three challenges facing the internet. Berit is a member of Global Shapers, the World Economic Forum's international network of young leaders; and serves on the boards of environmental media nonprofits Yes! Magazine and InvestigateWest.

Copyright © 2020 Strategic News Service. Redistribution prohibited without written permission.

I would like to thank Berit Anderson for her deep dive into the complicated topic of climate change and its effects on the insurance industry. I also want to thank Editor-in-Chief Sally Anderson for putting all of these thoughts into perfect shape.

Your comments are always welcome. Sincerely, Mark R. Anderson CEO

To arrange for a speech or consultation by Mark Anderson on subjects in technology and economics, or to schedule a strategic review of your company, email mark@stratnews.com. We also welcome your thoughts about topics you would like to suggest for future coverage in the SNS Global Report. For inquiries about Partnership or Sponsorship Opportunities and/or SNS Events, please contact Berit Anderson, SNS Programs Director, at berit@stratnews.com.

Please visit www.stratnews.com/insideSNS for:

Join us for four days of industry-changing conversations, problem-solving with global leaders, lively debates, and social events. And you'll connect with the world's most strategic thinkers and doers on tech, business, climate, and the global economy.

We look forward to returning to

Where's Mark? * On April 23, Mark will be hosting the newly minted annual FiReSide NYC, again at the magnificent Lotte New York Palace Hotel. (See details at the top of this issue.) * On October 6-9, 2020, he will be hosting the 18th annual Future in Review Conference, at The Lodge at Torrey Pines in La Jolla, California. Register now for the year's best rate: www.futureinreview.com.

"Strategic News Service," "SNS," "Future in Review," "FiRe," "INVNT/IP," and "SNS Project Inkwell" are all registered service marks of Strategic News Service LLC. ISSN 1093-8494 | ||||||||||||||

Berit Anderson is director of programs for Strategic News Service and FiRe events. Previously, she co-founded and served as the CEO of Scout.ai, a media company exploring the future of technology through analysis, science fiction, and scenario planning games.

Berit Anderson is director of programs for Strategic News Service and FiRe events. Previously, she co-founded and served as the CEO of Scout.ai, a media company exploring the future of technology through analysis, science fiction, and scenario planning games.